Contents

English

- Health insurance helps cover the cost of hospital treatment. However, newer policies also require us to bear part of the costs. The primary reason for this is to balance sufficient coverage with affordable premiums.

- Co-insurance and deductibles are the two main concepts where customers share part of the hospital bill. Co-insurance is a percentage of the total bill, while a deductible is a fixed amount that must be paid before the insurance covers the rest.

- Deductibles can help reduce our monthly premiums because we bear some of the risk of treatment costs. With AIA, there are now several deductible options, including the new ones: RM0/RM300 (available for existing customers only), RM500, RM500 SMART, RM500 + 20% coinsurance (capped at RM20k), and RM20k deductible.

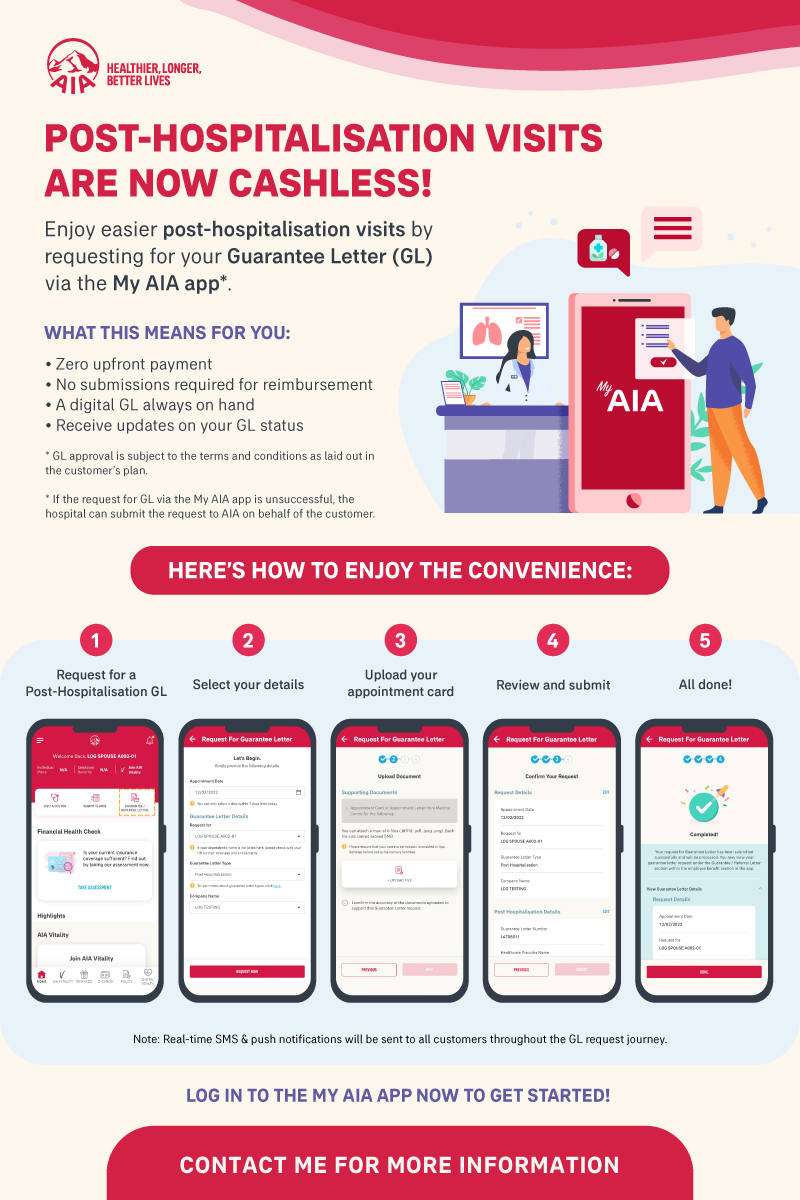

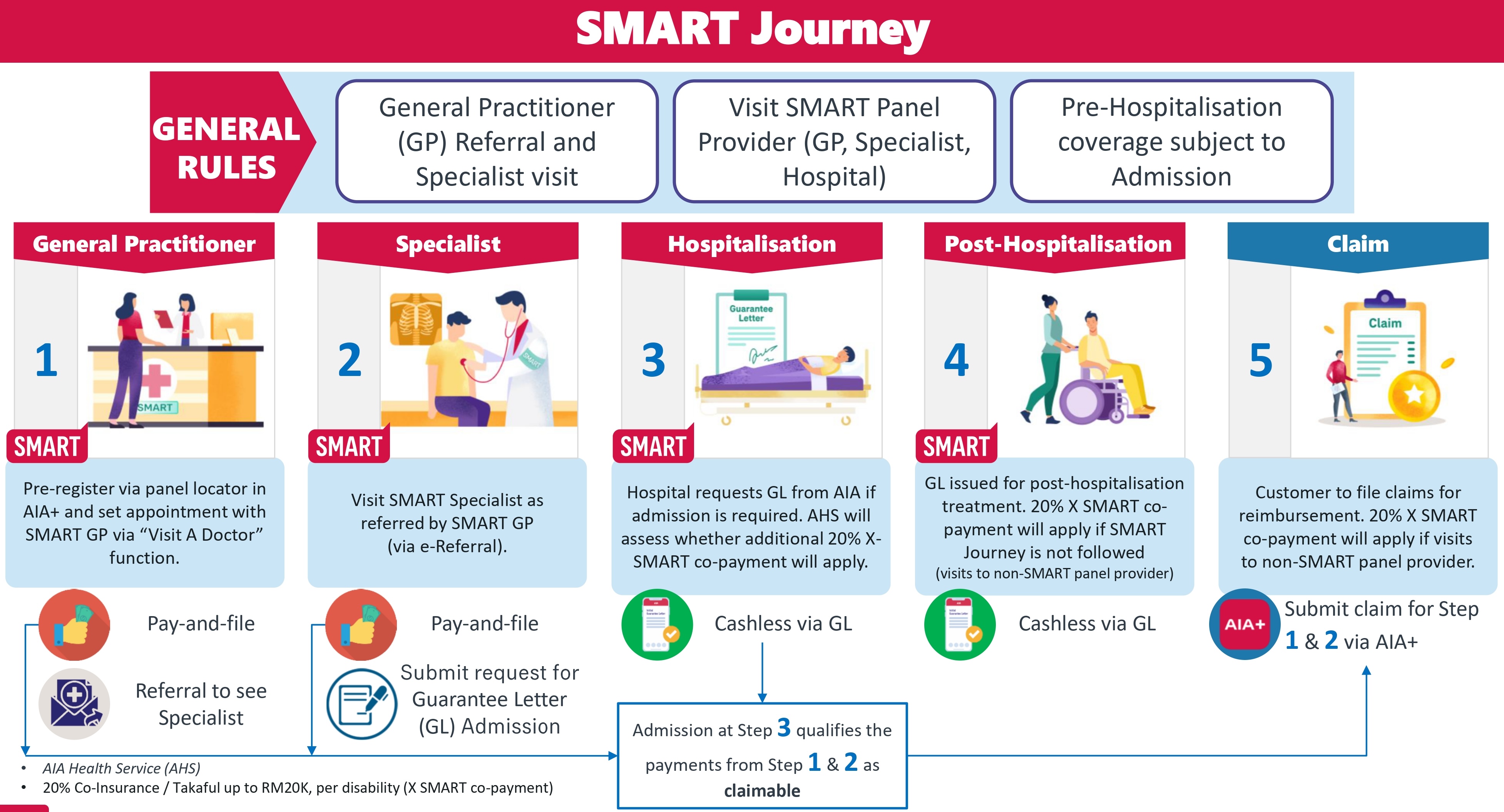

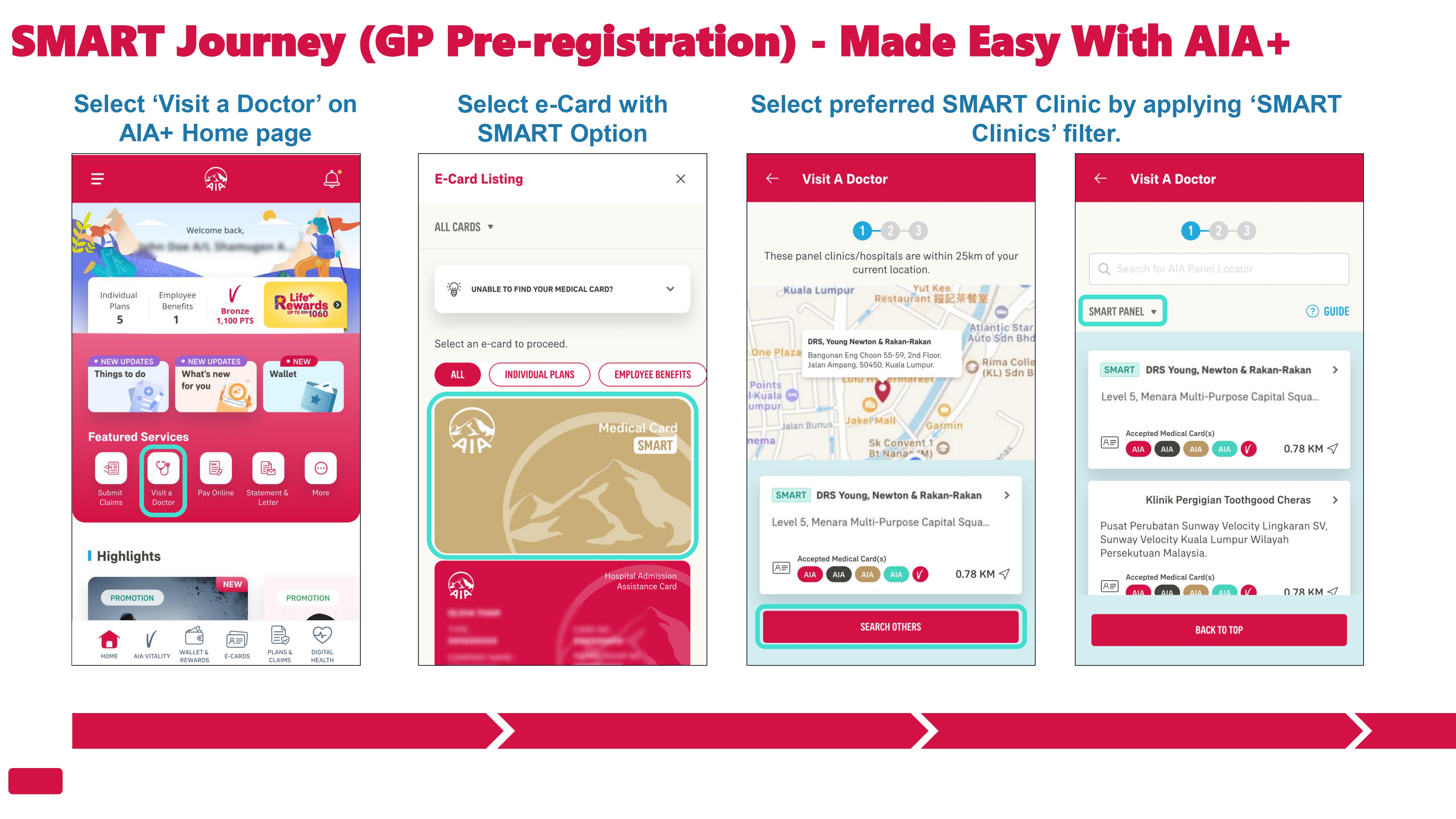

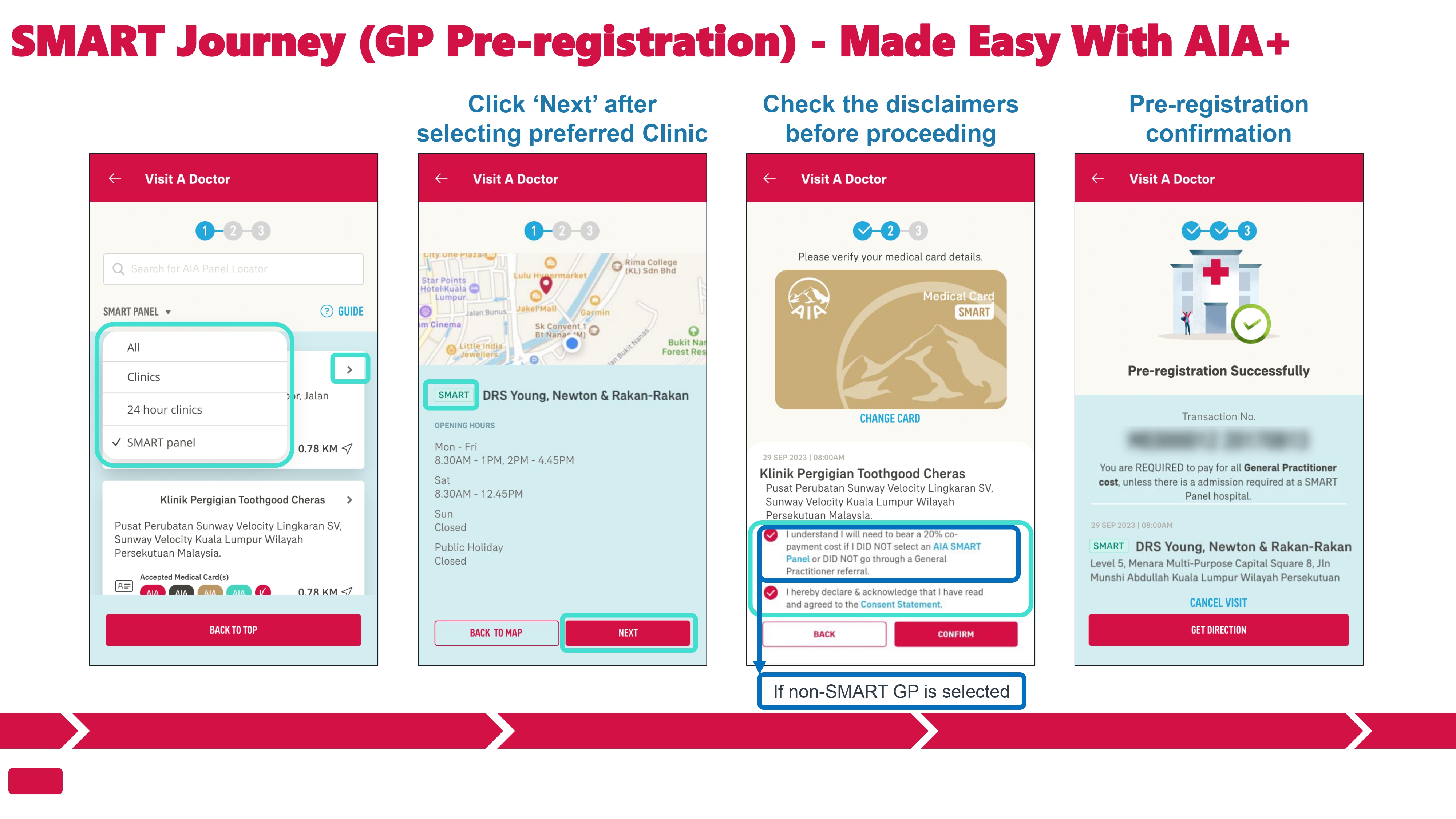

- For the RM500 SMART option, please refer to the following table and infographic to understand how it works. This SMART deductible operates differently depending on the type of treatment received and whether a SMART panel is consulted.

| Deductible | Notes |

|---|---|

| RM0/RM300 | For existing customers only |

| RM500 | Requires RM500 payment from the patient as part of the hospital bill |

| RM500 + 20% | Requires RM500 payment as part of the hospital bill, plus 20% of the total bill, capped at RM20k. Above RM20k covered by AIA 100% |

| RM20k | Requires RM20k payment from the patient as part of the hospital bill. Usually taken by those who have group insurance by employer |

| RM500 SMART (new customers) | Requires RM500 payment from the patient as part of the hospital bill, AND |

Requires visits to SMART panel GP & specialist before admission, except for emergencies. Otherwise, the 20% copayment will be imposed on top of the RM500 deductible.

| See how it works in the images below (see heading SMART DEDUCTIBLE) | ||

| SMART Option (only for existing customers who wish to reduce premium/contribution) | Requires visits to SMART panel GP & specialist before admission, except for emergencies. Otherwise, the 20% copayment will be imposed. |

| See how it works in the images below (see heading SMART DEDUCTIBLE) |

Bahasa Malaysia

- Kad medical membantu membayar kos rawatan di hospital. Walau bagaimanapun, polisi-polisi baru memerlukan kita membayar sebahagian dari kos tersebut. Sebabnya mengapa ia wujud adalah untuk mengekalkan keseimbangan antara perlindungan yang mencukupi dan kos caruman yang berpatutan.

- Co-insurans dan deductible adalah dua konsep utama di mana pelanggan membayar sebahagian dari bil hospital. Co-insurans adalah peratusan dari jumlah bil, manakala deductible adalah jumlah tetap yang perlu dibayar sebelum insurans menanggung selebihnya.

- Deductible boleh membantu mengurangkan caruman bulanan kita kerana kita menanggung sebahagian dari risiko kos rawatan. Di AIA, ada beberapa pilihan deductible, termasuk yang baru iaitu RM0/RM300 (hanya untuk pelanggan sedia ada), RM500, RM500 SMART, RM500 + 20% co-insurans (maksimum RM20k), dan deductible RM20k.

- Untuk pilihan RM500 SMART, sila rujuk jadual dan infografik berikut untuk memahami bagaimana ia berfungsi. Deductible SMART ini beroperasi dengan cara yang berbeza bergantung kepada jenis rawatan yang dan sekiranya panel SMART dikunjungi.

| Deduktibel | Nota |

|---|---|

| RM0/RM300 | Untuk pelanggan sedia ada sahaja |

| RM500 | Memerlukan pembayaran RM500 daripada pesakit sebagai sebahagian daripada bil hospital |

| RM500 + 20% | Memerlukan pembayaran RM500 sebagai sebahagian daripada bil hospital, serta 20% daripada jumlah bil, dihadkan pada RM20k. Jumlah selepas RM20k di-cover oleh AIA sepenuhnya |

| RM20k | Memerlukan pembayaran RM20k daripada pesakit sebagai sebahagian daripada bil hospital. Biasanya diambil oleh mereka yang mempunyai insurans berkumpulan oleh majikan |

| RM500 SMART | Memerlukan pembayaran RM500 daripada pesakit sebagai sebahagian daripada bil hospital, DAN |

Memerlukan lawatan ke GP panel SMART & pakar sebelum kemasukan ke hospital, kecuali untuk kecemasan. Jika tidak, 20% pembayaran bersama (copayment) akan dikenakan di atas deduktibel RM500.

| Lihat bagaimana ia berfungsi dalam imej di bawah |

SMART DEDUCTIBLE

- Please see the info below. Let me know if you have questions. There are more images of examples of how the copayment will be imposed if the steps are not followed. To avoid confusion, I will do away with sharing of those other images here unless necessary (via whatsapp).

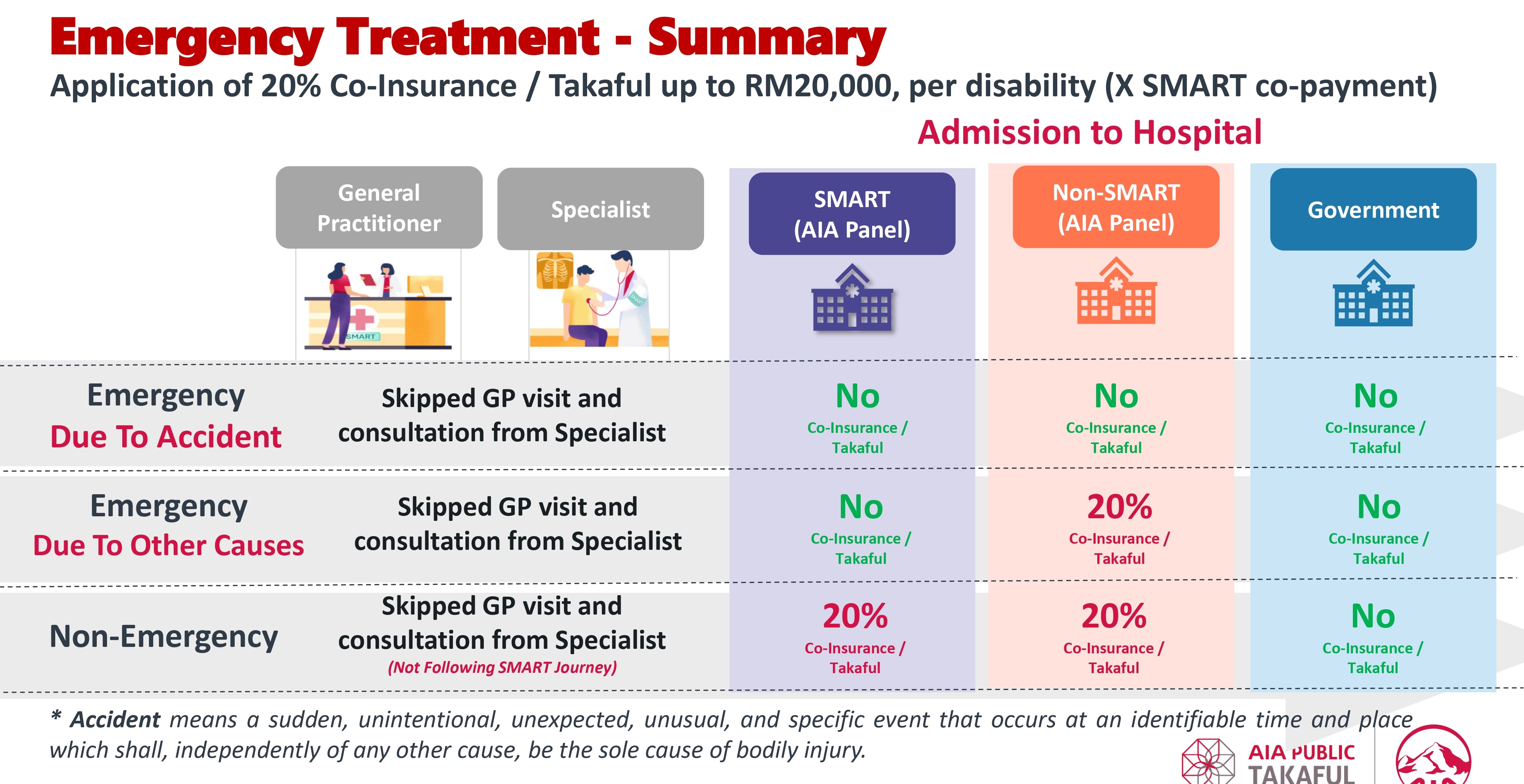

Definition of emergency

- Emergency Treatment means treatment in the event whereby immediate medical attention for preservation of life or limb is required for Disability which are sudden and severe failing which will be life threatening or lead to serious deterioration of health.

- Upon admission, an Initial Guarantee Letter shall be issued with X SMART Co-Insurance/Takaful applied. After treatment is done, AIA will issue a Final Guarantee Letter (FGL) based on the diagnosis of the SMART Medical Practitioner. If the illness/condition indeed requires Emergency Treatment, then the FGL will be issued with RM500 Deductible only, else, X SMART Co-Insurance/Takaful shall apply.

- Emergency Treatment at a Non-SMART Panel Provider shall be subjected to X SMART Co-Insurance/Takaful. For Emergency Treatment due to Accident only, AIA will waive the X SMART Co-Insurance/Takaful regardless of type of hospital.

- What are the examples of conditions that require Emergency Treatment?

Examples of common conditions/symptoms requiring Emergency Treatment (The list is not exhaustive and not limited to):

- Accidental injuries (Burns/Falls/Drowning/Poison ingestion/Electrocution etc.)

- Orthopedic emergencies (Hip fractures/Compartment Syndrome/Spine fracture/Limb amputation etc.

- Extensive burns (> than 25% body surface area) or involve facial region. Vascular injuries/major bleeding.

- Stroke/Brain Injury/Transient Ischemic Attacks.

SMART Panel List

SMART_Panel_Provider_Listing_v25f3a332e-2a1c-487f-b4fe-0816c97dda08.pdf

]]>